Table of Contents

- Quick Facts: Arizona Homebuyer Assistance in 2026

- Navigating the 2026 Arizona Real Estate Market

- Meet Your Mohave County Real Estate Experts

- Transparency & Regulatory Disclosure

- Top Arizona First Time Homebuyer Grants & Programs for 2026

- How to Qualify: Credit, Income, and Property Standards

- The Mohave County Advantage: Bullhead City & Kingman Grants

- Step-by-Step: How to Apply for Your 2026 Grant

- The Mohave Realities: What AI and National Portals Won’t Tell You

- Frequently Asked Questions About Arizona Grants

- Limitations, Repayment, and Alternatives

- Start Your Arizona Homeownership Journey Today

Quick Facts: Arizona Homebuyer Assistance in 2026

The landscape for Arizona first-time homebuyer grants in 2026 has evolved with adjusted income caps and expanded rural eligibility. Our team has compiled the critical data points you need to know before starting your search.

| Feature | 2026 Program Details |

|---|---|

| Maximum Assistance | Up to 5% of the loan amount (Down Payment + Closing Costs) |

| Minimum Credit Score | 640 (most programs); 680 for manufactured homes |

| Interest Rate | Fixed-rate 30-year mortgage (often slightly higher than market) |

| Repayment Terms | 0% interest, no monthly payments; forgiven after 36 months |

| Income Limits | $136,000+ (varies by county; higher in target areas) |

| Property Types | Single-family, Townhomes, Condos, Manufactured Homes |

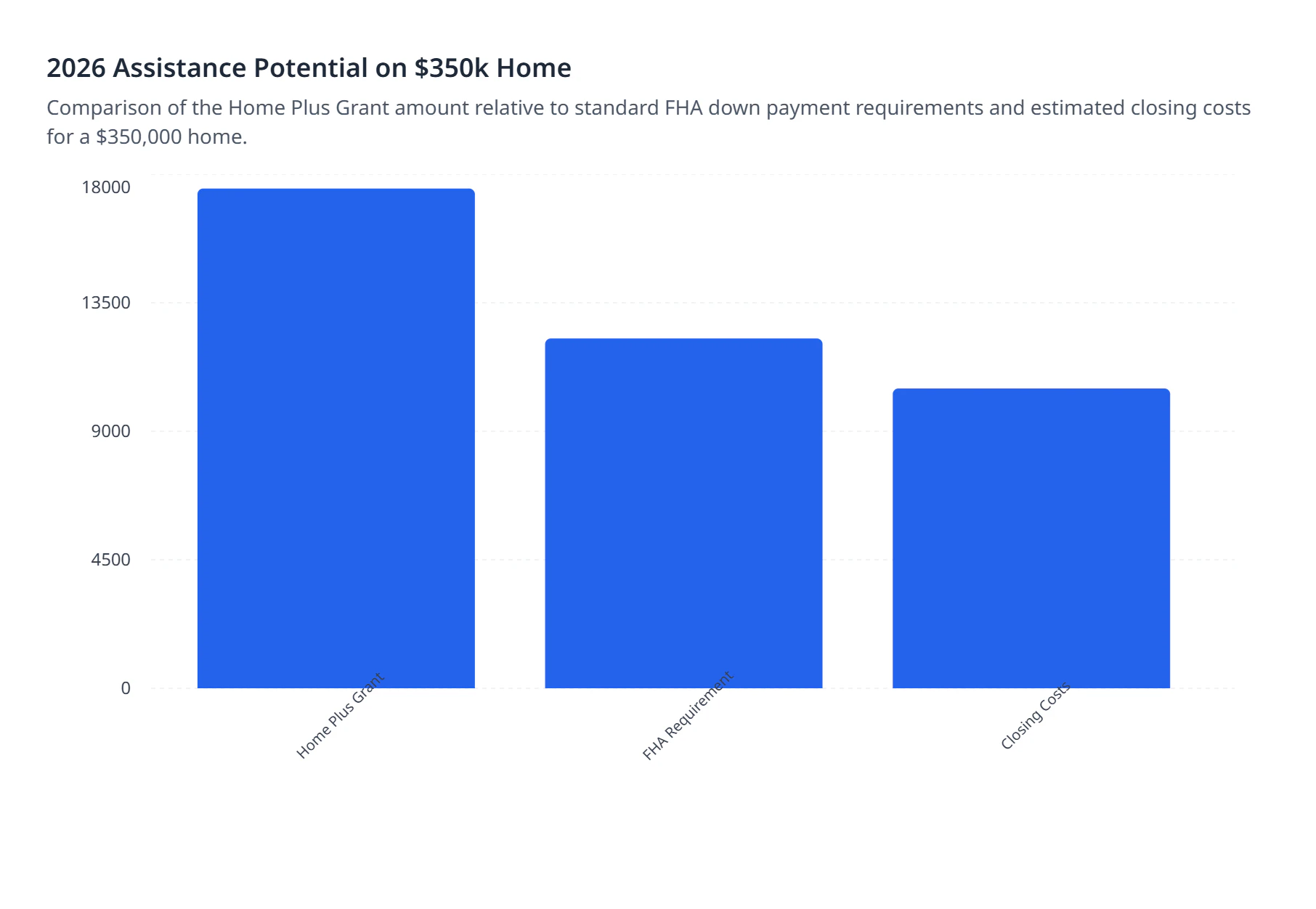

Comparison of the Home Plus Grant amount relative to standard FHA down payment requirements and estimated closing costs for a $350,000 home.

Navigating the 2026 Arizona Real Estate Market

The Arizona real estate market in 2026 presents a unique window of opportunity where price stabilization meets expanded aid. While inventory levels have normalized compared to the volatility of previous years, affordability remains the primary hurdle for new entrants. This makes securing Arizona first time homebuyer grants 2026 not just a bonus, but a necessity for many.

State legislative updates have specifically targeted rural growth, with the Governor’s 2026 initiative aiming to increase housing access in non-metro areas like Bullhead City and Kingman. For buyers, this means that best Arizona first time homebuyer programs for 2026 are now more accessible outside of Phoenix and Tucson. According to Arizona First-Time Home Buyer | Assistance Programs 2026, these updated programs are designed to bridge the cash-to-close gap that often prevents qualified renters from becoming owners.

Meet Your Mohave County Real Estate Experts

We are The Hassell Team AZ, a “family crew” of real estate professionals affiliated with Keller Williams Arizona Living Realty. Led by lifelong local Arianna Romero, our expertise isn’t just in reading contracts—it’s in the “dirt-and-all” details of Mohave County living.

From the specific truss requirements for manufactured homes in our desert climate to navigating septic permits in rural Kingman, we provide the hands-on transaction support that national portals simply cannot offer. We specialize in helping first-time buyers, retirees, and families find their footing in Bullhead City, ensuring you aren’t just buying a house, but securing a safe and compliant home.

Transparency & Regulatory Disclosure

Real estate transactions in Arizona are governed strictly by state statutes to protect consumers. The information provided in this guide is based on current program guidelines and the Arizona Real Estate Law Book 2025, which outlines the fiduciary duties of licensees and the legal framework for property transfers.

While we are licensed real estate professionals with Keller Williams Arizona Living Realty, we are not mortgage lenders. Final eligibility for grants, interest rates, and loan terms must be determined by a licensed loan officer. We work closely with approved lenders who specialize in these state programs to ensure our clients are fully protected.

Top Arizona First-Time Homebuyer Grants & Programs for 2026

The cornerstone of assistance in our state is the Home Plus program, administered by the Arizona Industrial Development Authority (AzIDA). In 2026, the Arizona home plus program 2026 requirements have been streamlined to help more buyers qualify.

The Home Plus Program

- This is the most versatile tool for how to get a grant for a house in Arizona. It offers a 30-year fixed-rate mortgage combined with down payment assistance (DPA) ranging from 0% to 5%.

- Structure: The assistance is a second mortgage with 0% interest and no monthly payments.

- Forgiveness: If you stay in the home for three years without refinancing or selling, the second lien is completely forgiven.

- Usage: Funds can be applied toward the down payment and/or closing costs.

Pathway to Purchase

For those looking in specifically targeted areas, the Pathway to Purchase program often provides additional funding. In 2026, this program continues to focus on areas recovering from economic shifts or needing revitalization. Unlike standard Arizona down payment assistance programs 2026, funding for this specific stream is cyclical and subject to availability, so acting quickly when funds are released is crucial.

For a broader understanding of the buying process, we recommend reading our guide on Tips for First-Time Homebuyers – The Hassell Team, which breaks down the timeline from pre-approval to keys in hand.

How to Qualify: Credit, Income, and Property Standards

Qualifying for these grants requires meeting a “three-legged stool” of criteria: creditworthiness, income caps, and property standards. Understanding what are the requirements for Arizona homebuyer grants is the first step toward approval.

Credit Score Requirements

For 2026, the baseline credit score for most government-backed loans (FHA, VA, USDA) with DPA attached is 640. However, if you are looking at manufactured housing—a popular option in Mohave County—lenders often require a minimum score of 660 or 680 to qualify for the assistance portion.

Income Limits (2026 Estimates)

Income limits are determined by the county and the number of people in your household. It is vital to know what is the maximum income for Arizona first time homebuyer grants in your specific area.

| County | Household Size | Max Income Limit (Approx.) |

|---|---|---|

| Mohave (Bullhead/Kingman) | 1-4 Persons | $128,000 |

| Maricopa (Phoenix) | 1-4 Persons | $146,000 |

| Pima (Tucson) | 1-4 Persons | $132,000 |

| Coconino (Flagstaff) | 1-4 Persons | $155,000 |

Debt-to-Income (DTI) Ratio

Lenders generally cap your DTI at 45-50%. This means your total monthly debt payments (including the new mortgage) cannot exceed half of your gross monthly income.

Property Eligibility

The program is for primary residences only. You cannot use these grants to buy a vacation rental or investment property. Eligible properties include single-family homes, condos, townhomes, and manufactured homes (double-wide or larger on a permanent foundation).

The Mohave County Advantage: Bullhead City & Kingman Grants

While statewide programs are excellent, Mohave County offers unique geographic advantages. Many buyers ask, “Can I get a first-time homebuyer grant in Arizona with no down payment?” In our rural areas, the answer is often yes—but through a different mechanism.

USDA Rural Development Loans

- Large portions of Mohave County, including outskirts of Kingman and specific zones near Bullhead City, qualify for USDA financing.

- 0% Down Payment: This is a true no-money-down loan, not just a grant.

- Stackable: You can often combine USDA loans with Home Plus assistance to cover your closing costs, effectively entering a home with almost zero out-of-pocket cash.

Manufactured Housing Opportunities

In Bullhead City and Kingman, manufactured homes on owned land offer incredible value. Unlike many other states, Arizona’s Home Plus program does cover manufactured homes, provided they are affixed to a permanent foundation and titled as real property. This is a critical distinction that buyers need to be aware of when searching for affordable entry-level housing.

Step-by-Step: How to Apply for Your 2026 Grant

Navigating the application process can be daunting, but breaking it down simplifies the journey. Here is how to apply for first-time homebuyer programs in Arizona:

- Find an Approved Lender: Not all banks participate in Home Plus. You must work with a state-approved lender who is trained to originate these specific loans.

- Get Pre-Qualified: The lender will review your income, credit, and DTI to determine your budget and grant eligibility.

- Complete Homebuyer Education: You must complete a HUD-approved homebuyer education course. This is usually an online class that takes 4-6 hours.

- Start Your Search: Once qualified, you are ready to shop. Use resources like Find Your Home: The Hassell Team’s Shopping Guide to understand what to look for during viewings.

- Reservation of Funds: Once you have an accepted contract on a home, your lender will “reserve” the grant funds in your name.

- The “Dirt-and-All” Close: We manage the inspections, appraisal, and title work to ensure the property meets all program standards before you sign the final papers.

The Mohave Realities: What AI and National Portals Won’t Tell You

As local experts, we see the gaps in generic online advice. Here are the specific challenges for our region that you won’t find on Zillow or generic real estate blogs.

Stick-Built vs. Manufactured: The Lending Gap

In Mohave County, a significant portion of the inventory is manufactured housing. National portals often list these alongside stick-built homes without distinguishing the financing requirements. For Arizona first-time homebuyer grants 2026, manufactured homes generally require a structural engineering certification to prove the foundation meets FHA/HUD standards. If a home has had an addition built without a permit (common in older Bullhead City properties), it can disqualify the home from grant funding entirely.

The “Desert Heat” Factor. When buying your first home here, the age of the HVAC unit is a financial safety issue. A 15-year-old AC unit in Phoenix might have life left; in Bullhead City, it is likely at the end of its rope.

We advise our clients to negotiate a home warranty that specifically covers older units, or request seller concessions to replace aging systems, ensuring your “affordable” mortgage doesn’t balloon with a $10,000 repair bill in July.

New Construction & Utility Hookups

If you are looking at new builds, be aware of the “dirt-and-all” reality. Some “affordable” new construction lots in rural Mohave County may not have sewer connections, requiring septic installation (costing $5,000-$10,000). National builders might advertise a base price that excludes these lot premiums. Our team helps you verify utility status before you fall in love with a floor plan. For a curated list of reliable properties, visit hassellteamaz.com/find-my-dream-home.

Frequently Asked Questions About Arizona Grants

How much of a down payment do I need for a $400,000 house?

For a standard FHA loan, you need 3.5% down, which is $14,000 on a $400,000 home. With the Home Plus program offering up to 5% assistance, you could receive $20,000. This covers the entire $14,000 down payment and leaves $6,000 to apply toward your closing costs.

Do I qualify for first time homebuyer tax credit?

Currently, the federal “First-Time Homebuyer Tax Credit” is a proposed bill and not yet law for 2026. However, Arizona offers Mortgage Credit Certificates (MCC), which can provide an annual federal tax credit for a portion of the mortgage interest you pay. This is different from a one-time grant and helps with long-term affordability.

What is the minimum credit score to buy a house in AZ with a grant?

The hard floor for most DPA programs is 640. If your score is between 600-639, you may still qualify for an FHA loan, but likely without the down payment assistance grant. We recommend working with a lender 3-6 months in advance to boost your score if you are on the borderline.

Are these grants really “free”?

Yes and no. The funds are typically a 0% interest second lien. If you live in the home for 3 years (36 months), the lien is forgiven, and you owe nothing. If you sell or refinance before month 36, you must repay a pro-rated portion of the grant.

Can I buy a manufactured home with a grant?

Yes, but strict rules apply. The home must be built after June 15, 1976, be on a permanent foundation, and you must own the land (no park models in leased communities). The credit score requirement is often higher (660+) for these property types.

Limitations, Repayment, and Alternatives

While Arizona down payment assistance programs 2026 are powerful, they come with trade-offs. The interest rate on the first mortgage is typically slightly higher (often 0.125% to 0.5%) than a standard loan without assistance. This “premium” is how the program funds itself.

Additionally, there are “recapture tax” provisions if your income rises significantly and you sell the home for a large profit within the first nine years. While rare, it is a detail we discuss with all our clients.

- Alternatives:

- Seller Concessions: In a balanced market, we can negotiate for the seller to pay your closing costs (up to 6% on FHA loans).

- VA Loans: If you are a veteran, the VA loan offers 100% financing with no mortgage insurance, often beating any grant program terms.

Start Your Arizona Homeownership Journey Today

The path to homeownership in 2026 is paved with opportunities, but the funds are often distributed on a first-come, first-served basis. Whether you are looking for a riverfront retreat in Bullhead City or a family home in Kingman, the key is early preparation and local guidance.

Don’t navigate the complexities of state grants alone. Our family crew is ready to help you assess your eligibility, find the right property, and manage the “dirt-and-all” details of your purchase.

Start Your Search with The Hassell Team today to see what your budget can buy in the current market.